Using Land and Buildings as Collateral in Scotland

1. Taking Security Interest in Real Property in Scotland

In Scotland, taking security interest in real property (land and buildings) is a fundamental element of secured lending. While the concept is broadly akin to the mortgage system used in England and elsewhere, Scots law distinguishes itself by deploying a distinct legal framework, terminology, and processes.

This article offers a detailed exploration of using land and buildings as collateral in Scotland, including how security over land is created, managed, and enforced. We will cover the relevant statutory framework, the practical steps involved in taking security as collateral, how ranking and priorities are managed, and the nuances of enforcement.

The basic goal is to provide a comprehensive overview for lenders, solicitors, borrowers and other secured finance professionals seeking to understand Scottish property law with respect to collateral security.

2. The Statutory Basis: Standard Security Under Scots Law

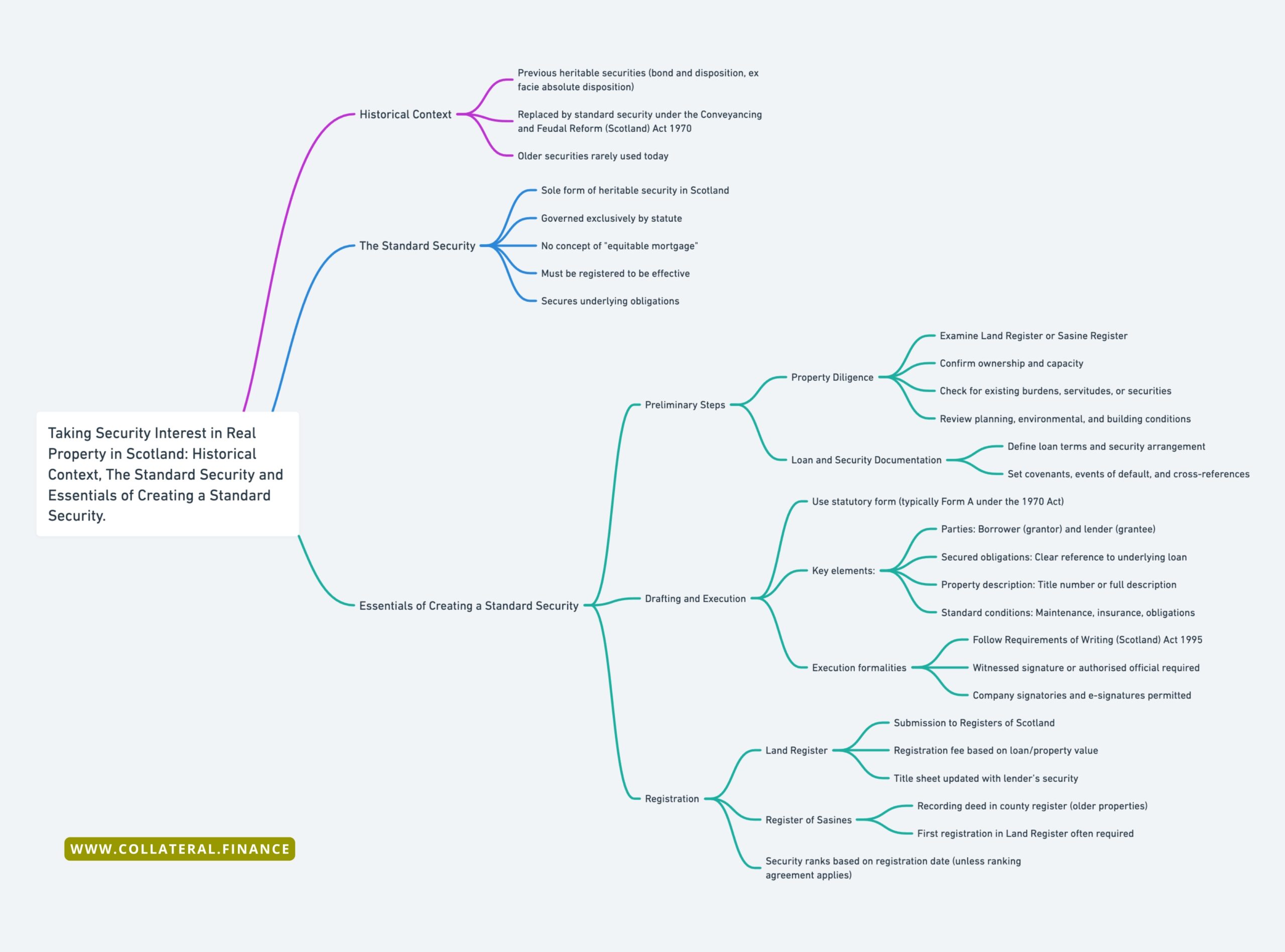

2.1 Historical Context

Prior to modern reforms, Scots law recognised various forms of heritable security—most notably the bond and disposition in security and the ex facie absolute disposition—to secure debts against property.

These instruments often conveyed ownership to the creditor subject to redemption by the debtor. Over time, complications with these forms led to legislative intervention, culminating in the creation of the standard security under the Conveyancing and Feudal Reform (Scotland) Act 1970 (the “1970 Act”).

Sections 9 and 10 of the 1970 Act formally abolished or restricted many of the older security devices, although a small number remain extant under transitional provisions.

2.2 The Standard Security

Under Section 11 of the 1970 Act, the standard security is now the only competent form of heritable security over land in Scotland for new lending.

Conceptually, it is akin to a mortgage in other jurisdictions; however, its statutory nature dictates the manner of its creation, form, and enforcement.

As observed in Dick v Clydesdale Bank (1986) S.C. (H.L.) 184, the courts emphasise strict adherence to the statutory framework when scrutinising validity and ranking of securities.

Key points to note:

- Statutory Form: The 1970 Act prescribes mandatory wording for the creation of a valid standard security. Schedule 2 of the Act sets out several forms (Forms A and B) which may be used (with adaptations) in practice.

- Registering the Security: To create a security interest in real property in Scotland, the security must be registered in the Land Register of Scotland or, in rarer cases, the Register of Sasines (for titles not yet on the Land Register). Unlike English law, there is no concept of “equitable mortgage” in Scots law: a security must be registered to be effective.

- Underlying Obligation: The standard security secures one or more underlying obligations (e.g., repayment of a loan). If the underlying obligation is repaid or otherwise extinguished, the security no longer has effect.

3. Essentials of Creating a Standard Security

3.1 Preliminary Steps

Property Diligence

Before drafting a standard security, lenders and their solicitors undertake thorough due diligence to confirm the viability and value of the property.

This process typically includes:

- Examining Title: Reviewing the property’s title sheet in the Land Register of Scotland, or (for older titles) checking the Register of Sasines. This confirms the borrower’s legal ownership and capacity to grant security. The principle that a real right in land only vests upon registration is underpinned by the Land Registration (Scotland) Act 2012.

- Checking Burdens and Servitudes: Identifying any burdens (e.g., restrictive conditions) under the Title Conditions (Scotland) Act 2003 or servitudes (similar to easements) that might restrict use or negatively affect marketability.

- Prior Securities: Verifying existing standard securities or floating charges, as these may impact the ranking and priority of the proposed security.

- Planning and Environmental Matters: Ensuring that valid planning permissions, building warrants, and environmental certifications are in place, particularly for commercial or high-value properties.

Loan and Security Documentation

Once property diligence is complete, lenders and borrowers negotiate the terms of the loan—often documented in a facility agreement or similar finance contract.

Key commercial terms, covenants, and events of default will be reflected in the standard security. For instance, any negative pledge clause (prohibiting additional security) or financial covenant will be cross-referenced in the security deed to avoid ambiguity if enforcement becomes necessary.

3.2 Drafting and Execution

Under the 1970 Act, a standard security must substantially conform to one of the statutory forms—usually Form A in Schedule 2. This ensures the security is recognised by law and provides clarity for both parties. Key drafting elements include:

- Parties: The borrower (grantor) and the lender (grantee). Corporate borrowers must also comply with the Companies Act 2006 requirements for registering charges at Companies House within 21 days.

- Description of the Secured Obligations: A precise statement of the debt or obligations being secured, generally referencing the facility agreement.

- Property Description: The deed must accurately identify the property, typically by its Land Register title number. If unregistered, a full Sasine description (including boundaries) is required.

- Standard Conditions: Section 11 and Schedule 3 of the 1970 Act set out default conditions relating to property maintenance, insurance, and remedies on default. Parties can vary these conditions if agreed in writing.

- Execution Formalities: As governed by the Requirements of Writing (Scotland) Act 1995, valid execution usually entails the borrower’s signature in the presence of a witness. Alternatively, for companies, two authorised signatories or a director’s signature (witnessed) may suffice. Electronic signatures are increasingly recognised if they meet statutory criteria.

3.3 Registration

Registration is essential to create a security interest in real property. If the security remains unregistered, it may be ineffective against third parties or in insolvency. The key registers are:

- Land Register: Most properties are now on this register. An application (including the executed standard security and a registration form) is submitted to Registers of Scotland along with the prescribed fee. Section 50 of the Land Registration (Scotland) Act 2012 confirms that registration perfects the real right, which is critical for ranking and enforcement.

- Register of Sasines: Less common today, but if the property has not yet undergone first registration, the deed is recorded in the county’s Sasine register. However, any subsequent transfer or significant transaction typically triggers first registration in the Land Register.

Upon registration, the standard security ranks from the date and time it is submitted (the “date of presentation”).

If multiple securities are registered over the same property, they generally rank in order of submission unless a ranking agreement alters this priority.

Notably, case law such as Royal Bank of Scotland v Wilson [2010] UKSC 50 highlights the strict adherence to statutory notice and registration procedures, underlining the importance of precise compliance.

4. Ranking and Priority of Security Interests in Land

4.1 The Importance of Ranking

In many secured finance transactions, multiple lenders may hold securities over the same property. This can arise when a borrower takes out additional loans from different lenders, or even multiple loans from the same lender.

Ranking refers to the order in which each lender’s claim will be paid out if the borrower defaults and enforcement action is taken.

For lenders, understanding ranking is crucial because it directly impacts the likelihood of recovering funds. A first-ranking creditor (sometimes called a “senior lender”) is paid in advance of second-ranking or “junior” creditors from the proceeds of any enforced sale.

This concept is underpinned by Scots property law, which aims to provide transparency and certainty for creditors and borrowers alike.

4.2 Default Rule: First in Time

Under Scots law, the principle of “first in time, first in right” determines the ranking of standard securities. This principle, often expressed in Latin as qui prior est tempore potior est jure, is generally recognised by the courts and codified through various property law statutes, including the 1970 Act.

Practically, once a standard security is registered in the Land Register of Scotland (or, less commonly, the Register of Sasines for older titles), its priority is set according to the exact date and time of registration.

For example, if Standard Security A is registered at 10:00 a.m. and Standard Security B is registered at 2:00 p.m. on the same day, Standard Security A takes priority and will be paid first in any enforcement.

This approach is intended to provide clarity and prevent disputes over who should be recognised first. This simply means a senior lender will often insist on completing registration promptly to secure an undisputed first-ranking position over the property.

4.3 Ranking Agreements

There are circumstances where the natural “first in time” rule does not reflect the commercial reality of a deal—particularly when a borrower seeks additional capital, or when multiple lenders agree to share or adjust their relative security positions.

In such cases, the parties can enter into a ranking agreement, sometimes called a deed of postponement or deed of alteration of ranking. These agreements are permitted under Section 13 of the 1970 Act and allow an existing first-ranking lender to postpone or regulate its interest in favour of another lender.

For example, a lender that already holds a standard security may consent to becoming second-ranking if a new lender provides further funding that benefits all parties (e.g., development finance that increases the property’s overall value).

Importantly, a ranking agreement must also be registered in the Land Register to be effective against third parties.

Without registration, the altered ranking would not be publicly recognised, which could lead to disputes or confusion during enforcement.

Proper registration and drafting of ranking agreements is therefore essential to avoid complications if a borrower defaults and the property is sold to repay outstanding debts.

5. Practical Considerations for Lenders

5.1 Certificates of Title

Before completing a secured loan transaction in Scotland, lenders typically obtain a “certificate of title” from a Scottish solicitor to confirm that the borrower holds valid title to the property.

This certificate, governed by professional regulations and practice standards, scrutinises the Land Register to verify ownership, boundaries, and any encumbrances.

In accordance with the 1970 Act, the solicitor’s report also addresses whether the property is subject to encumbrances (e.g., servitudes, title conditions, or restrictions) that could influence its value.

The certificate provides comfort that the standard security, once executed in compliance with the Requirements of Writing (Scotland) Act 1995, will be valid. It further confirms that, upon registration, the lender’s security interest will be adequately perfected and ranked. This is especially critical in multi-lender financings where priorities must be clearly established to avoid future disputes.

In practice, lenders rely on this certificate as evidence of good title and as a safeguard against potential title defects that may compromise the security’s enforceability.

5.2 Negative Pledges and Non-Disturbance

To protect the lender’s collateral, finance documents frequently include negative pledge clauses, which contractually prevent the borrower from granting additional security interests over the same asset without the lender’s prior consent.

Although not expressly codified in Scots statute, negative pledge provisions are widely used in loan agreements to preserve the lender’s priority position and protect against competing security interests.

In commercial developments or multi-tenant scenarios, lenders may also require non-disturbance agreements with tenants, ensuring existing leases remain in force if the lender enforces its security under sections 19–24 of the 1970 Act.

By maintaining tenants in possession, the property’s rental income can be preserved, thus upholding its capital value for the benefit of the lender and any subsequent purchaser.

5.3 Company Grantors

When the borrower is a limited company registered in Scotland, the lender must also comply with Part 25 of the Companies Act 2006, which requires the particulars of any charge (including a standard security) to be registered with Companies House within 21 days of its creation.

Failure to register on time renders the security void against a liquidator, administrator, or creditor of the company, although it remains enforceable between the contracting parties.

This step is crucial to ensure the lender’s security is recognised in any insolvency scenario, thereby safeguarding recovery prospects and reinforcing the lender’s secured status.

6. Enforcement of a Standard Security over Land

6.1 Default and the Lender’s Right to Enforce

Under Scots law, when a borrower (or “debtor”) fails to meet obligations under a loan agreement—by missing payments, breaching covenants, or becoming insolvent—the lender (or “creditor”) can enforce its rights under the 1970 Act.

The 1970 Act outlines statutory procedures that lenders must follow before taking possession of, or selling, the secured property.

A key Scottish case clarifying calling-up notice requirements is Royal Bank of Scotland Plc v Wilson [2010] UKSC 50, which reinforced the necessity of serving valid statutory notices prior to repossession.

6.2 Court Involvement and Pre-Action Requirements

When the secured property is the borrower’s home, legislation such as the Home Owner and Debtor Protection (Scotland) Act 2010 adds further protections. These rules reflect a policy of ensuring repossession is a last resort and that borrowers have an opportunity to remedy defaults.

Specifically, lenders must comply with pre-action protocols before raising court proceedings. Such protocols generally require the lender to:

- Provide the borrower with clear information on their arrears and the total sum due.

- Make reasonable attempts to reach an alternative arrangement (e.g., revised payment schedules).

- Advise the borrower to seek independent debt advice.

If these pre-action steps are not followed, a court may refuse to grant an order permitting repossession or sale.

In many residential cases, the lender must obtain a court order under section 24 of the 1970 Act before exercising repossession rights. Failure to do so could invalidate the process.

In contrast, purely commercial properties (e.g., offices or warehouses) do not usually trigger these additional homeowner protections, so lenders may proceed without the same degree of judicial oversight.

6.3 Methods of Enforcement

If the borrower does not remedy the default within the statutory notice period, or if they fail to respond to the lender’s efforts to seek a workable solution, the lender may escalate enforcement in several ways:

- Calling-Up Notice: A calling-up notice, under section 19 of the 1970 Act, formally demands repayment of all sums secured by the standard security. This notice typically provides a two-month window for repayment. If the borrower fails to pay within that time, the lender can proceed with further action, including repossession or seeking court authority to sell.

- Notice of Default: Under section 21 of the 1970 Act, the lender may serve a notice of default if it does not wish to demand full repayment. This notice specifies the nature of the default (for example, failure to maintain insurance or breaching a loan covenant) and gives the borrower at least one month to rectify it.

- Voluntary Surrender: In certain situations, the borrower may agree to surrender the property without court involvement. This approach can benefit both parties by speeding up the process and potentially reducing legal costs. However, the lender should ensure the borrower’s consent is documented to avoid later disputes.

- Right of Sale: The most common enforcement route is for the lender to sell the property to recover the outstanding debt. Under section 25 of the 1970 Act, the lender can apply to the court to exercise the power of sale (if court permission is required) or sell the property directly (for purely commercial properties or if all requirements have otherwise been satisfied).

- Foreclosure (Rare in Scotland): While strict foreclosure is conceptually possible in Scots law, it is exceptionally uncommon. Lenders generally opt to sell the property, as foreclosure would involve the lender becoming the owner outright, which is rarely the preferred commercial route.

- Receiver or Administrator (Corporate Borrowers): Where the debtor is a company and the standard security extends to substantially all of the company’s assets, the lender may seek to appoint an administrative receiver—although the Enterprise Act 2002 greatly restricted the use of administrative receiverships. More commonly, a lender or other creditors might initiate administration to restructure or realise the company’s assets.

6.4 Sale Process and Good Faith

When exercising a power of sale, the lender must act in good faith and take reasonable steps to secure the best available price for the property (see section 25 of the 1970 Act and the statutory conditions in Schedule 3).

This duty protects the borrower and any subsequent creditors, ensuring that the property is not sold at a gross undervalue.

Practically, lenders often instruct surveyors to value the property and estate agents to market it appropriately. Failure to act in good faith could result in legal challenges, particularly if the borrower or a subsequent creditor alleges that the sale proceeds were reduced due to negligence or bad faith. If a sale does proceed, the lender applies the net proceeds to the outstanding debt, with any surplus returning to the borrower.

Conversely, if a shortfall remains after the sale, the lender may pursue the borrower personally for the balance (subject to any insolvency procedures or contractual limitations).

7. Discharge and Repossession of Security Interests in Land

7.1 Discharge of the Security

When a borrower fully repays or refinances the debt secured by a standard security, the security must be discharged to clear the property title of any encumbrance.

Under section 17 of the 1970 Act, a lender (the “creditor”) grants a formal discharge deed confirming that the obligations secured under the standard security have been satisfied in full. This deed is then registered in the Land Register of Scotland.

The discharge document usually follows a succinct statutory form. It identifies the original security, references the relevant title or title number, and states that all sums due have been paid or otherwise settled.

Once registered, the Land Register (or Register of Sasines) is updated to remove the standard security from the property title, effectively restoring the borrower (the “debtor”) to unencumbered ownership.

This process is crucial as it eliminates the creditor’s real right in security. In practical terms, the borrower or a new lender (in a refinancing scenario) will typically pay a legal fee and a modest registration fee for recording the discharge.

This step is essential not only for clearing the borrower’s title but also for ensuring transparency in future transactions. Borrowers often require a formal discharge before selling or further refinancing the property, as an un-discharged security might deter prospective lenders or purchasers.

7.2 Repossession and Aftermath

In the event of borrower default—such as missed repayments or breach of other obligations under a loan agreement—the creditor may enforce the standard security in accordance with the 1970 Act.

Following the prescribed notice procedures (often through a Calling-Up Notice under section 19), the lender may repossess and sell the secured property.

Residential protections are enhanced by the Home Owner and Debtor Protection (Scotland) Act 2010, which ensures court oversight and compliance with pre-action protocols.

Once the property is sold, the lender applies the net sale proceeds toward the secured debt. This includes repayment of the outstanding capital, accrued interest, and reasonable enforcement expenses, consistent with Standard Condition 12 of Schedule 3 to the 1970 Act.

Where more than one creditor holds a security over the same property, distribution follows the established ranking, usually by registration date or by agreement.

Any surplus after settling all secured debts and costs is returned to the borrower (or, if insolvent, to the borrower’s insolvency practitioner).

If the proceeds are insufficient to clear the outstanding balance, the lender may pursue the shortfall on an unsecured basis, subject to any limitations or arrangements set out in the underlying finance documentation or insolvency law.

8. Special Topics and Developments

8.1 Floating Charges Over Land

In Scottish law, floating charges are governed primarily by the Companies Act 2006 (Part 25) and can only be granted by certain legal entities such as companies and LLPs.

A floating charge is different from a fixed security because it “floats” over a changing pool of assets—this may include land, movable property, and other assets—until a defined event of crystallisation occurs (e.g., the appointment of an administrator or liquidator under the Insolvency Act 1986).

Crucially, a floating charge over heritable property (land) in Scotland does not create a real right over the land until crystallisation. Before that point, the borrower remains free to deal with the property, subject to any contractual restrictions in the finance documentation.

If crystallisation occurs, the floating charge becomes a fixed charge, attaching to the relevant assets as they stand at the time of crystallisation. However, if another lender has taken a standard security over the same land—registered under the 1970 Act—that standard security ranks ahead of any floating charge.

As a result, many lenders prefer a standard security to ensure immediate and robust protection over real estate.

From a practical standpoint, lenders seeking security in Scotland often take both a standard security (covering the land) and a floating charge (covering other assets such as stock or receivables).

This combination ensures comprehensive security across the borrower’s asset base, while preserving the priority of a fixed security over real estate should the borrower encounter financial distress.

8.2 Cross-Border Transactions

Many finance transactions involving Scottish property are cross-border—for instance, an English bank lending to a company or LLP with assets north of the border.

In these scenarios, it is essential to remember that Scots property law is distinct from the law of England and Wales. Specifically:

- Lex Situs Rule: Security over land is governed by the law of the country where the property is located. Therefore, the creation, validity, and enforceability of security over Scottish land must comply with Scots law.

- Formality Requirements: The Requirements of Writing (Scotland) Act 1995 lays down execution formalities. Loan and security documents must be validly executed (often with a Scottish law governed standard security deed) and registered in the Land Register of Scotland or, rarely, the Register of Sasines.

- Local Legal Advice: Lenders typically instruct Scottish counsel to draft or review standard securities, ensure compliance with registration procedures, and provide certificates of title or legal opinions. Such local expertise helps prevent defects in the security that might weaken the lender’s protection.

8.3 Recent Trends and Regulatory Considerations

- Land and Buildings Transaction Tax (LBTT): LBTT applies to property purchases rather than the creation of securities. However, under the Land and Buildings Transaction Tax (Scotland) Act 2013, complexities can arise if a finance transaction is structured to involve a transfer of ownership or if there is a corporate reorganisation. Lenders should be alert to LBTT implications when properties are transferred to special purpose vehicles (SPVs) or during refinancing deals.

- Registers of Scotland Digital Services: The Registers of Scotland continues to modernise its platforms, offering digital submissions for certain property transactions. Over time, these developments should streamline registration of standard securities and discharges, reducing turnaround times and administrative costs.

- Environmental, Social, and Governance (ESG): Growing ESG pressures mean lenders increasingly factor in energy efficiency, environmental risk, and social impact when underwriting loans secured on Scottish property. Legislation such as the Climate Change (Scotland) Act 2009 underlines the Scottish Government’s commitment to sustainability, prompting finance providers to carry out deeper due diligence on a property’s environmental profile, planning constraints, and community considerations. This trend is especially relevant for large-scale commercial developments, where a property’s sustainability credentials may directly affect its valuation and marketability.

9. Practical Tips for Lenders and Practitioners

- Engage Scottish Solicitors Early: Given the distinctive nature of Scots law, especially regarding the standard security under the 1970 Act, it is crucial for English or foreign lenders to engage Scottish legal counsel from the outset. Scottish solicitors are experienced with local procedural nuances and can help avoid drafting errors, ensure compliance with statutory forms, and guide you through the registration process.

- Confirm the Correct Title: Before proceeding, verify the property’s title in detail. This is particularly important for properties moving from the Register of Sasines to the Land Register. A meticulous title search not only confirms ownership but also identifies any pre-existing encumbrances—such as burdens or servitudes—that might affect the security’s priority. This diligence minimises future disputes and aligns with established property law principles.

- Monitor Execution Requirements: Strict adherence to the Requirements of Writing (Scotland) Act 1995 is essential. Ensure that all execution formalities—signatures, dates, and witness attestations—are correctly observed. A lapse in these requirements can render a security deed unenforceable, potentially jeopardising the lender’s position in a default scenario.

- Use Statutory Forms: The standard security deed must conform substantially to the statutory forms laid out in the 1970 Act. While it is acceptable to incorporate additional bespoke clauses, the core statutory language must remain intact to ensure legal certainty and enforceability.

- Don’t Forget Companies House: For corporate borrowers, the security interest must be registered with Companies House within 21 days, as required by the Companies Act 2006 . Failing to meet this deadline can result in the security being void against a liquidator or administrator, thus weakening the lender’s recovery position in insolvency.

- Obtain Ranking Agreements When Needed: In cases where multiple securities exist over the same property, negotiating a ranking agreement is essential. Such agreements clearly define the order of priority and should be registered to be effective against third parties. This step is especially important if additional funding is sought later.

- Plan Enforcement Carefully: Plan your enforcement strategy in advance. Whether opting for a calling-up notice under the statutory regime or initiating court proceedings (particularly for residential properties under the 2010 Act, having a clear plan ensures that enforcement actions are carried out efficiently and fairly.

- Protect Your Collateral and Stay Updated: Regularly review the property’s insurance coverage and maintain thorough records. Additionally, stay informed about any legislative or case law developments that may impact secured lending. This proactive approach helps safeguard your collateral and ensures compliance with regulatory reforms and standards.

10. Conclusion

Taking security over land in Scotland is a relatively streamlined, statute-driven process under the auspices of the 1970 Act. The standard security is the essential tool for lenders, providing robust protection and a clear route to enforcement should the borrower default.

However, the unique legal framework demands careful attention to formalities, including:

- Properly drafting and executing the standard security using the statutory forms.

- Registering in the correct Scottish property register (Land Register or Sasines).

- Observing ranking rules and registering any necessary ranking agreements.

- Complying with post-registration requirements such as registration at Companies House for corporate borrowers.

- Following statutory notice procedures before enforcement, particularly where residential property or consumer protection rules apply.

Borrowers, for their part, benefit from transparent, well-regulated security arrangements that facilitate access to finance while safeguarding key borrower protections.

As with any secured transaction, engaging knowledgeable Scottish counsel, conducting thorough due diligence, and adhering to strict statutory requirements remain the keys to a successful lending arrangement in Scotland’s property market.